Cosors, my views on short selling are quite similar. Far more negatives than any positive (if any) from such a practice. If only Aust followed South Korea’s path….

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

The Talga Bar

- Thread starter cosors

- Start date

Yes, the timeframe it’s taken to get an answer from the Swedish Supreme Court sucks the proverbial c$&!, however that is the process in Sweden, and as our trusting MD stated in recent Quarterly Investor Webinar, we must respect the process.It feels like it’s taking longer than it should to throw out the case and I’m getting anxious …

More recently someone from “the other place” noted they received notification from, no doubt, an admin monkey from the Supreme Court and they stated that appeals decisions can take 1 to 4 months. We are not there yet.

Many on this forum and “the other place” initially speculated 1 month for the process however that is categorically incorrect. If it were the case we’d have an answer and TLG and it’s lawyers would’ve been very aware of that timeframe from the outset, which they weren’t.

Maybe I’m too optimistic, after all I do think the sun shines out of my backside at times, but these final appeals will be squashed certainly before end Q1 ‘24 and more than likely before mid Feb ‘24 if not much sooner. TLG management wouldn’t be silly enough to only want to raise $15m now if they thought it would take much longer as the SP will drop to the floor well before then.

In the meantime kickback and if you’re bored visit “the other place” every now and then for a laugh. The sitting of the pot by some of the drop kicks over there is beyond hilarious. It is funny stuff if you’re not threatened by their dribble.

Onwards and upwards to us all.

Semmel

Top 20

There are some special kind of individuals over at hot crapper, that's for sure  ..

..

On a different note, I am very positively surprised about how well the share price is holding up so far. Fingers crossed this continues!") time to get some ground covered here.. literally and figuratively!

time to get some ground covered here.. literally and figuratively!

..On a different note, I am very positively surprised about how well the share price is holding up so far. Fingers crossed this continues!

time to get some ground covered here.. literally and figuratively! cosors

👀

https://thestockexchange.com.au/threads/permits.4987/post-274241

@beserk I searched for this picture because I had it from your post in my mind.

A perfect topic for the bar:

And just because we up here with the Norrbotten region (Kiruna/Vittangi) know the topic over the years, oppression, genocide and colonialism. The same approach now in the Israel conflict from FFF, extended by further untruths.

I don't know if you are as aware of the topic of Greta and Israel or Palestinians Down Under as we are here. We have a special sensitisation when it comes to anti-Semitism. The international FFF movement and Greta herself have now repeatedly used anti-Semitic stereotypes about Israel and Jews. Most recently, Greta was at a really big demonstration in Amsterdam few days ago and was interrupted by a climate activist because he wanted to talk about the climate and not politics.

She didn't care and joined in a chant whose meaning and background I still don't understand, she probably doesn't either:

Greta to 70,000 demonstrators: There is no climate justice on occupied land!

I think some of our Sami see it the same way. Here is an extract from an interview here in Germany with a staunch opponent (Sami) of us:

Speaker: Can you talk about the history of the colonisation of Sápmi, the area inhabited by Sámi? How does this colonisation continue today with the so-called "green transition" - or eco-colonialism? (!!! this statement comes from a person who works for a radio station that is partly financed by public money)

...

Speaker: Who does the land belong to?

N. J. A.: To the people who have preserved it for generations. It is theirs, and belongs to their children and grandchildren and their great-grandchildren and the generations that will live there afterwards.

...

All indigenous people in the world understand nature better than the colonisers.

Think about who, according to this idea, are all colonisers around the world today. Personally, I think that's pretty radical.

I am not posting any more of this interview as it is pure propaganda and has nothing to do with balanced journalism. You Australians are now responsible for this suffering, genocide and oppression.)

I have it in my head that the Sami do not own the land, they are users ~in front of the Crown. I mention that the identical narrative of occupied land, i.e. colonialism, is the same in both topics, whether for some of the FFF or some of the Sami. Greta's behaviour in this terrible conflict now makes me better understand her behaviour with the 300 wind turbines that are to be demolished. Or other things she fights or demonstrates against on the basis of incomplete knowledge. Perhaps she should have spent more time at school. Maybe then she would know that the land does not belong to the Sami and that Israel is not an apartheid/segregation state, even if Amnesty would like it to be. And here the circle closes from Palestinians to Sami via Amnesty.

-> I know you and your family are Sami yourself and certainly have a different view and probably feel less or not oppressed or colonised.

However, the press is full of this topic and also the fact that the left has also partly joined the ranks of the anti-Semites (Marx 'The Jewish question'). That's why I personally find it surprising that the big socialist newspaper here is now turning its back on Greta. I only mention this because I read a lot of media from different camps and it's a big issue for the conservatives at the moment. When it first started there was nothing in the left-wing press about FFF, but there was in the conservative press the more. I always try to stay in the centre. In any case, Greta has now become too much for the biggest socialist newspaper and she has been declared persona non grata in their editorial. Here is a condensate in this context, translated:

"Poor Greta worshippers

Thunberg's disciples appalled by heroine*

The unfortunate admirers of Sweden's leading climate activist are currently weeping bitter tears into their weather vanes. While Greta Thunberg was declared the "heroine of our time" or "ambassador of conscience" years ago and was the cover girl of a new youth movement in all the world's media, it now turns out that the blonde Northerner is a stone-cold anti-Semite after she once again fell into anti-Semitic stereotypes at a demonstration in Amsterdam at the weekend. "How dare she?" the Greta worshippers shriek in despair and horror at their heroine's fall from grace. In future, the beheaded woman will probably no longer be regarded as the "voice of a new generation" and invited to international conferences. No high-ranking figure from politics and society would allow themselves to be photographed with an anti-Semite at their side - except perhaps Alice Weidel (proven far-right party)! But who will take over Thunberg's legacy? Sahra Wagenknecht (currently founding a new party and causing the Left to collapse)? Alice Schwarzer (women's rights activist or feminist)? Women for Future.

The Gretaists have really earned it with their heroine worship."

https://taz.de/Archiv...

*I had to look it up: in Greek mythology this refers to the female heroes in German "Heroinen" singular the heroine (in our country the separation of the sexes in language is more important to many than switching on the mind). It means Greta as a female demigod.

wiki

That happens with cults of personality and when it's no longer about the cause.

Last edited:

Sorry, I didn't mean to interrupt. It took me a while to press send. One round for you!

Sorry, I didn't mean to interrupt. It took me a while to press send. One round for you!cosors

👀

Since the ASX messages no longer work properly here I sometimes visit HC. Disadvantage without an account: I can only see each post individually. And since I can't put anyone on ignore it's often a pain. I limit myself to reading the posts with a high rating. But I've got so used to the amenities here that I don't miss anything over there.Yes, the timeframe it’s taken to get an answer from the Swedish Supreme Court sucks the proverbial c$&!, however that is the process in Sweden, and as our trusting MD stated in recent Quarterly Investor Webinar, we must respect the process.

More recently someone from “the other place” noted they received notification from, no doubt, an admin monkey from the Supreme Court and they stated that appeals decisions can take 1 to 4 months. We are not there yet.

Many on this forum and “the other place” initially speculated 1 month for the process however that is categorically incorrect. If it were the case we’d have an answer and TLG and it’s lawyers would’ve been very aware of that timeframe from the outset, which they weren’t.

Maybe I’m too optimistic, after all I do think the sun shines out of my backside at times, but these final appeals will be squashed certainly before end Q1 ‘24 and more than likely before mid Feb ‘24 if not much sooner. TLG management wouldn’t be silly enough to only want to raise $15m now if they thought it would take much longer as the SP will drop to the floor well before then.

In the meantime kickback and if you’re bored visit “the other place” every now and then for a laugh. The sitting of the pot by some of the drop kicks over there is beyond hilarious. It is funny stuff if you’re not threatened by their dribble.

Onwards and upwards to us all.

Besides, I still can't stand TMH and the system. I wouldn't be surprised if they have special deals for shorter and their paid troll avatars.

Last edited:

cosors

👀

"Press onto the tube with hydrogen paste

Hydrogen is considered a key element of the energy transition. In the transport sector, however, use has so far been limited to larger vehicles with pressure tanks. Researchers from the Fraunhofer Institute in Dresden have now developed a method with which hydrogen can be bound into a paste under normal pressure - non-explosive and versatile. In the future, the “power paste” will be used in particular to power small vehicles such as e-scooters.The power paste from the tube can be used to produce gaseous hydrogen when it comes into contact with water. Many applications are conceivable. Photo: Fraunhofer IFAM

What are the benefits of hydrogen paste?

Entire sectors of industry are pinning their hopes on hydrogen; many experts consider the highly combustible gas to be the fuel of the future. Hydrogen is also increasingly showing its potential in the transport sector. Because with hydrogen in the tank, not a gram of carbon dioxide is produced, only water vapor. However, it is complex to use - simply because of the fact that hydrogen tanks in fuel cell vehicles have to withstand a pressure of 700 bar. For comparison: a car tire has a pressure of 2.5 bar.Hydrogen paste, on the other hand, significantly simplifies the use of hydrogen to power vehicles. The researchers from the Fraunhofer Institute for Manufacturing Engineering and Applied Materials Research (IFAM) in Dresden have a trick: They use magnesium to bind hydrogen to it. Magnesium is one of the most common elements and is easily accessible. The result is a mass reminiscent of toothpaste. In order to operate a vehicle with it, the hydrogen-containing paste can come from a replaceable cartridge, for example. While driving, a stamp presses the required amount of paste out of the cartridge. Only after adding water does the gaseous hydrogen arise, which ultimately generates electricity for the drive in a fuel cell.

A big advantage of hydrogen paste is its stability, which allows it to be stored for years. “With our hydrogen paste, hydrogen can be chemically stored at room temperature and ambient pressure and released again as needed,” explains Dr. Marcus Vogt, scientist at IFAM. The hydrogen paste is perfect for small vehicles in particular – it is light, easy to transport and can be replaced quickly.

The refueling process is extremely simple: Instead of going to a gas station, drivers of scooters or scooters, for example, simply change a cartridge and also fill tap water into a water tank - done. What's special: Only about half of the hydrogen produced on the vehicle comes from the paste, the other half comes from the water carried. It is not a problem if small vehicles equipped with hydrogen paste in the cartridge are left in the sun for hours in the summer heat, because hydrogen paste only decomposes above around 250 degrees Celsius.

What is hydrogen paste made of?

The starting material for hydrogen paste is powdered magnesium - one of the most common elements and therefore a readily available raw material. At 350 degrees Celsius and five to six times atmospheric pressure, the magnesium reacts with hydrogen to form magnesium hydride. Add esters and metal salt and the hydrogen paste is ready.Hydrogen paste is non-toxic, safe and has a very long shelf life. It is characterized above all by a very high energy density in relation to weight and volume. The energy content is more than ten times that of modern lithium-ion batteries.

Storing hydrogen in magnesium hydride offers the advantage that hydrogen does not have to be cooled significantly and compressed to 700 bar. Materials researchers at the Helmholtz Center in Geesthacht (HZG) have been working for several years on appropriate techniques to eliminate pressure tanks in fuel cell vehicles in favor of magnesium hydride tanks. The scientists from IFAM, on the other hand, are targeting small vehicles with their “power paste” from the cartridge.

What applications is hydrogen paste suitable for?

Hydrogen paste could not only extend the range of e-scooters and e-scooters. It could also be used in so-called range extenders in electric cars or delivery vehicles, where they could generate electricity via a fuel cell to increase the range. Drones could also be powered with it. With conventional batteries, the flight time is currently limited to a maximum of half an hour, with hydrogen paste it could be several hours - helpful, for example, for inspections with drones in the energy industry .Other application examples are conceivable: For example, the paste could provide the necessary energy for a refrigerator, coffee machine, heater or stove using a fuel cell when camping. Possible areas of application also include backup and emergency energy systems, portable electronic devices and chargers, sensors, probes and buoys. Due to the rapid availability of large amounts of energy, the low weight and the independence from the power grid, the technology is particularly suitable for grid-independent and mobile applications.

While gaseous hydrogen requires a costly infrastructure, hydrogen paste could also be used wherever such an infrastructure is lacking. “Any gas station could offer hydrogen paste in cartridges or canisters,” says researcher Dr. Marcus Vogt from IFAM.

When will the hydrogen paste come onto the market?

The development of the hydrogen paste is part of the H2PROGRESS project , which in turn is part of the HYPOS innovation project funded by the Federal Ministry of Education and Research (BMBF). In addition, the Federal Ministry for Economic Affairs and Energy (BMWi) is supporting the further development of the “Powerpaste” from the Fraunhofer Institute IFAM.

The institute would like to complete the construction of a production facility at the Fraunhofer Project Center for Energy Storage and Systems (ZESS) in 2023, where four tons of the hydrogen paste will be produced annually. The production facility was already planned for the end of 2021, but had to be postponed due to the pandemic and the war in Ukraine. Now the IFAM scientists would like to push the envelope to advance the use of hydrogen paste and test it in detail."

https://www.enbw.com/unternehmen/eco-journal/wasserstoffpaste.html

The only comment here is: It is true that magnesium is common, but it is currently a scarce raw material and classified as critical raw material (90% comes from China). But if a circular economy is built in it might work. The energy density and how much energy has to be put into it is of course an open question for me. Nevertheless, all alternatives that are conceivable in practice and not just in theory are helpful I think.

I don't know if you've noticed. Sweden will go back into nuclear power with full force. They expect demand to rise from the 5TWh to 75TWh in 2045. You know that most Swedes don't like wind turbines and are fighting against them everywhere. The minister who initiated this behind the back of the government coalition is the environment minister and at 27a the youngest ever.

I don't know if you've noticed. Sweden will go back into nuclear power with full force. They expect demand to rise from the 5TWh to 75TWh in 2045. You know that most Swedes don't like wind turbines and are fighting against them everywhere. The minister who initiated this behind the back of the government coalition is the environment minister and at 27a the youngest ever.As additional information it is perhaps interesting to know that the largest project for the small reactors or mini-reactors has failed. The costs were almost twice as high and so it was no longer worthwhile.

Last edited:

Semmel

Top 20

Lol nice article on the paste, but that is neither energy efficient not practical for EVs. There MIGHT be an application for drones if it provides a weight advantage.. but you would need the paste and water to be stored on there, then you need a fuel cell to use the hydrogen.

To me this looks like a solution im search of a problem... Or in other words, a typical research grant result. It's not bad per se and something cool might come from this some day, but I wouldn't hold my breath..

To me this looks like a solution im search of a problem... Or in other words, a typical research grant result. It's not bad per se and something cool might come from this some day, but I wouldn't hold my breath..

Proga

Regular

I think it's more to do with China announcing permitting. All graphite stocks are holding. It's still too early to know what China will actually do and the wests response. The West will respond and it will be beneficial for graphite stocks. They have no option.There are some special kind of individuals over at hot crapper, that's for sure

On a different note, I am very positively surprised about how well the share price is holding up so far. Fingers crossed this continues!

I posted this in the other place on the SYR thread today

https://www.fastmarkets.com/insights/market-welcomes-addition-of-synthetic-graphite-to-crma/

A couple of snippets:

Permitting is likely to become increasingly focused on technological developments to drive down carbon dioxide footprints of plans, according to Latour. “The EC and member countries will take some more information on processes and the technological route before authorizing permits to make sure that energy performance and material yields are state of the art, in order to ensure the lowest CO2 footprint by process design, not relying only on low CO2 electricity grids,” she said.

“We expect graphite demand in the European Union to exceed 500,000 tonnes by 2030 from the battery sector alone and half of this demand will be for synthetic graphite. Therefore, including synthetic graphite in the CRMA is an important step toward the development of a localized supply chain and reduce the EU’s dependency on imports of this critical raw material,” Georgiev said on Friday.

exceed 500,000 tonnes by 2030 is for AAM which means they'll need ~500,000 tonnes of natural concentrate to produce >250kt of natural AAM.

From the 1st paragraph, I've been rabbiting on about this for years as the next logical step. The EU isn't going to allow companies to set up with access to hydro (low CO2 electricity grids) and think it's hunky dory to use as much electricity as they like because they're meeting CO2 emissions. It's clean power laundering. EV's will need a lot of power from the grid to recharge so managing total grid usage will become a major issue if not already. Managing and monitoring industry power usage will become just as important as CO2 emission.

The EU and US aren't going to do a China and only use 20% natural in the anode mix. The power required is too great. If anything, they'll want to see the natural mix as high as possible. The ability to build natural AAM manufacturing plants will be the limiting factor. Not mining natural graphite concentrate. Especially in the short to medium term.

Last edited:

Semmel

Top 20

500ktpa Graphite anode seems way too low. That's just 10M cars (assuming an average of 50kg per car which translates to about 50kWh pack) per year. This is a very conservative assumption, and it doesn't I include stationary storage and trucks, busses, etc. I would be quite surprised if the actual number is not 3 to 4 times higher.

WheresTheMonkey

Regular

Good to see a bit of optimism from you. I know you are an expert on the state of graphite but sometimes reading your posts over at the other place I do detectI think it's more to do with China announcing permitting. All graphite stocks are holding. It's still too early to know what China will actually do and the wests response. The West will respond and it will be beneficial for graphite stocks. They have no option.

......................................................

The EU and US aren't going to do a China and only use 20% natural in the anode mix. The power required is too great. If anything, they'll want to see the natural mix as high as possible. The ability to build natural AAM manufacturing plants will be the limiting factor. Not mining natural graphite concentrate. Especially in the short to medium term.

WheresTheMonkey

Regular

500ktpa Graphite anode seems way too low. That's just 10M cars (assuming an average of 50kg per car which translates to about 50kWh pack) per year. This is a very conservative assumption, and it doesn't I include stationary storage and trucks, busses, etc. I would be quite surprised if the actual number is not 3 to 4 times higher.

Market data international

In 2022, 11.3mn new vehicles were registered on the European passenger car market, around 4% fewer than in the previous year. This means that there was no recovery from the pandemic-related declines of the two previous years

cosors

👀

In China, VW and BMW have serious sales problems, there is talk of a flop. They have had to cut prices massively.Market data international

www.vda.de

In 2022, 11.3mn new vehicles were registered on the European passenger car market, around 4% fewer than in the previous year. This means that there was no recovery from the pandemic-related declines of the two previous years

Proga

Regular

Completely agree Semmel. It was my first reaction. Not many of those 10m will be hybrids by then so the ave battery size will be closer to 80KWh than 50. Maybe double but not 3 to 4 times higher. I use 1.2kg of anode per 1kWh500ktpa Graphite anode seems way too low. That's just 10M cars (assuming an average of 50kg per car which translates to about 50kWh pack) per year. This is a very conservative assumption, and it doesn't I include stationary storage and trucks, busses, etc. I would be quite surprised if the actual number is not 3 to 4 times higher.

Proga

Regular

Frustration. China lowering natural in the anode mix has stuffed things up for SYR. LiB production is 45% higher YoY which is what I was predicting in 2022. At the same anode mix of 2022, Balama would have been close to full production. Instead it's doing short production runs then shutting down. It's played havoc with the finances along with the natural graphite price.Good to see a bit of optimism from you. I know you are an expert on the state of graphite but sometimes reading your posts over at the other place I do detectpessimismfrustration at where things are at especially in the shorter term.

Balama at full production + the $220m grant would have easily paid for the 45kt AAM expansion at Vidalia. The FID would have been out and ordering of long lead time equipment would have been done. On the flip side, China was financing the competition.

Part of the problem is Tesla's fault when they started cutting prices but most is with the Chinese. It looks to be orchestrated. Interesting to note the Chinese announcement on banning exports didn't happen until they had their new 200kt natural graphite mine in operation. Most of the flake produced is battery grade. It's in the Heilongjiang province where most of China's fines come from.

It looks to me as China halved the natural anode mix from 2022 but the growth in 2023 is only 45% creating the deficit. If China keep the low mix and along with the new mine, they have enough natural battery grade graphite for a while.

I'm also trying to warn people things are going to be tough in the next 6-12 months until the West can start ramping up. If China revert back to the 2022 mix then happy days but I can't see it happening. Not with the banning threat. It has gone to far for backflips. So I'm hoping the US throws the kitchen sink at trying to ramp graphite AAM production. If they do, SYR is in position A as the first mover.

Semmel

Top 20

Proga, thx for that overview. We desperately lack this type of global awareness. I for one didnt know that China changed the anode mix. It makes sense, the natural anode from china is quite diverse and having less of it means higher quality, which is needed for EVs. At moment, China dictates the graphite mix in anodes. However, this might stop once serious production is ramping up outside china.

Proga

Regular

My pleasure.Proga, thx for that overview. We desperately lack this type of global awareness. I for one didnt know that China changed the anode mix. It makes sense, the natural anode from china is quite diverse and having less of it means higher quality, which is needed for EVs. At moment, China dictates the graphite mix in anodes. However, this might stop once serious production is ramping up outside china.

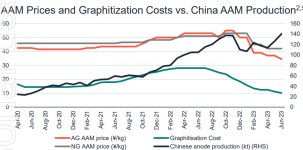

It goes a lot deeper. In the past 18 months, China has been rapidly expanding their synthetic manufacturing plants. And still are actually. They have enough capacity out to 2027/28. They have so much capacity atm their utilisation rates are at ~30% and none are making money at those utilisation rates. Due to the EV price war, a lot are using calcined pet coke which is cheap and low quality feed stock to try and make ends meet.

Below is the changes in prices between natural and synthetic AAM. The black line is AAM production both natural and artificial. There was a dip at the start of the year/end of last year so they did stockpile some but it's back up to historical highs. With production of batteries to October 45% higher than last year, the black line has continued on it's merry way upwards. Mostly synthetic unfortunately. The drop in graphitisation costs is when coke and natural flake prices started declining and the switch away from natural to the cheap and nasty stuff.

Don't buy an EV made in China in 2023. I've read reports where Chinese consumers are getting range anxiety. No wonder.

Attachments

WheresTheMonkey

Regular

So ok we are all waiting around for the permit decision,

we have all after many years have watched and waited for the “Transformational Year” come and go

and the SP is definitely going sub $1.00

And we wait

So where is everyone’s next holiday

Ours is spending a week with the hounds ( 2 x Maltese cross) staying right on the beach at North Avoca ( just north of Sydney quite close to where we live) plus with 4 friends we have known since our university days in February

Then a trip to Perth in April then a Pacific Cruise in June all next year

What are you doing or looking forward to even over Christmas whilst we all wait ?

we have all after many years have watched and waited for the “Transformational Year” come and go

and the SP is definitely going sub $1.00

And we wait

So where is everyone’s next holiday

Ours is spending a week with the hounds ( 2 x Maltese cross) staying right on the beach at North Avoca ( just north of Sydney quite close to where we live) plus with 4 friends we have known since our university days in February

Then a trip to Perth in April then a Pacific Cruise in June all next year

What are you doing or looking forward to even over Christmas whilst we all wait ?

Similar threads

- Replies

- 6

- Views

- 3K

- Replies

- 214

- Views

- 53K

- Article

- Replies

- 13

- Views

- 5K

- Replies

- 8

- Views

- 3K