You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

TLG Discussion 2022

- Thread starter zeeb0t

- Start date

WheresTheMonkey

Regular

cosors

👀

This reminds me of my first message that was moderated at the poison site. I meant how an avatar can give himself such a simple minded name after a watch.Is that Navitimer ?

WheresTheMonkey

Regular

Good to see a reasonable portion of the shorting has unwound in the lead up to the webinar

www.shortman.com.au

www.shortman.com.au

ShortMan - Short position graph for TLG

Short position graph and statistics for TLG

WheresTheMonkey

Regular

In fact I get the feeling the unwinding has been continuing all week if we look at the increased volumes and the upwards direction of the SPGood to see a reasonable portion of the shorting has unwound in the lead up to the webinar

ShortMan - Short position graph for TLG

Short position graph and statistics for TLG

WheresTheMonkey

Regular

OK so I am going to ask a general question that has me a bit puzzled. So Ecograf last night got it's approval from it's local municipal council to build it's PSG plant in Kwinana Western Australia. But they still do not have an operating mine which means they will be buying feed stock from other third party mines.

I would have thought that being the case that they would need to do OEM qualification every time they changed suppliers. Surely there must be some sort of process. I mean we are talking about expensive EVs perhaps. Maybe it could happen for smaller batteries of lower cost but surely not EVs which should last 10 years plus

Anyway just curious. Then again I guess the concentration process is pretty standard

As usual they are all over at Hot Crapper beating their chests telling the world how superior their company is compared to others chief amongst them being dopey Spid who runs for cover everytime you prove him wrong.

I would have thought that being the case that they would need to do OEM qualification every time they changed suppliers. Surely there must be some sort of process. I mean we are talking about expensive EVs perhaps. Maybe it could happen for smaller batteries of lower cost but surely not EVs which should last 10 years plus

Anyway just curious. Then again I guess the concentration process is pretty standard

As usual they are all over at Hot Crapper beating their chests telling the world how superior their company is compared to others chief amongst them being dopey Spid who runs for cover everytime you prove him wrong.

Slymeat

Move on, nothing to see.

Laws for environmental impact tracability do not yet exist, as far as I understand it—otherwise nobody would be able to,use anything from out of China or Africa, so they don‘t need to prove environmental impact from mine to finished product and I assume they will just need to be more diligent with the outward quality assurance checks of their product.

When laws for tracability do come in it may be another story. Although Europe, who was leading that charge, are delaying those laws now—probably been placed in the too hard basket.

Owning your own mine seems so much easier to prove environmental impact.

When laws for tracability do come in it may be another story. Although Europe, who was leading that charge, are delaying those laws now—probably been placed in the too hard basket.

Owning your own mine seems so much easier to prove environmental impact.

cosors

👀

In the beginning, some time ago, I found EGR interesting because they focused on three things. Then I got on my nerves that they made an official announcement out of every snippet of news. At that time I took a closer look at Talga and the approval process. I read the Fraser Mining Report and discovered that Tanzania the land of EGRsOK so I am going to ask a general question that has me a bit puzzled. So Ecograf last night got it's approval from it's local municipal council to build it's PSG plant in Kwinana Western Australia. But they still do not have an operating mine which means they will be buying feed stock from other third party mines.

I would have thought that being the case that they would need to do OEM qualification every time they changed suppliers. Surely there must be some sort of process. I mean we are talking about expensive EVs perhaps. Maybe it could happen for smaller batteries of lower cost but surely not EVs which should last 10 years plus

Anyway just curious. Then again I guess the concentration process is pretty standard

As usual they are all over at Hot Crapper beating their chests telling the world how superior their company is compared to others chief amongst them being dopey Spid who runs for cover everytime you prove him wrong.

resource was in the second last place of all I mean. A catastrophic statement to go with it. Then I looked closely at the situation on site. There is nothing, no perifery, purely nothing. Or I have searched wrong which I don't believe. Then came the action with land reservation at Northvolt. The SP spiked and I got out, had just a small parcel. Nevertheless, this was a borderline misdirection of the shareholders since they only had to ask NV once if they needed help with recycling. That was already clearly foreseeable. Apart from the fact that no one will earn any money with recycling for the foreseeable future, maybe five years. Nevertheless they made an official announcement with confetti: Behold! Ecograf and Northvolt!

But when the anode plant is finished and they have to buy their graphite from here or there then according to a standard I can imagine. Like this: CAS 7782-42-5. Then I imagine that also the shape must be clear. I guess that there are some specifications from the OEM but they then only have to prove that they obtain this or that material. I can imagine that this is possible but you are right it has to follow an established process. And they don't just change their supplier, today here tomorrow there. I can't imagine that at all.

Back when I was still reading in their Cold Crapper group no one went into the Fraser Report and the assessment of Tanzania as a mining country. That says a lot for me! No critical view. I searched the forum for it but didn't find a single comment. I got the impression that the To The Mooners doesn't care where it is mined. It will finally work out.)

I didn't want to spoil the fun and kept quiet. I only mentioned the NV thing here at TSE.

All in all I have the impression that EGR's marketing in front is great, but I don't like the behavior and view behind the scenes. This is not meant to be a downramp. It's just my experience and I can be wrong about some things. But I feel deceived with the NV move...

____

And they are an advertising customer of TMH/HC. You probably know what that means.

Last edited:

cosors

👀

I add:Syrah are building a PSG plant in Louisiana so their target is clearly USA. Sure it's not very environmentally friendly to ship it all the way from Africa but I don't think the constraints on that are as big in the USA or Asia as they might be in the EU.

"CATL Pushes Back American Battery Plant News Amid Pelosi's Taiwan Visit

...

It's important to note that CATL hasn't substantiated the anonymous claims. Tesla and Ford have also declined to provide statements."

https://insideevs.com/news/602248/china-catl-delays-us-battery-plant-news-pelosi-taiwan/

catdog

Member

As I understand it, PSG is not the same as Talnode-C. PSG is Purified Spheronised Natural Graphite. It still needs to be coated to produce the battery ready coated anode powder i.e active anode material.OK so I am going to ask a general question that has me a bit puzzled. So Ecograf last night got it's approval from it's local municipal council to build it's PSG plant in Kwinana Western Australia. But they still do not have an operating mine which means they will be buying feed stock from other third party mines.

I would have thought that being the case that they would need to do OEM qualification every time they changed suppliers. Surely there must be some sort of process. I mean we are talking about expensive EVs perhaps. Maybe it could happen for smaller batteries of lower cost but surely not EVs which should last 10 years plus

Anyway just curious. Then again I guess the concentration process is pretty standard

As usual they are all over at Hot Crapper beating their chests telling the world how superior their company is compared to others chief amongst them being dopey Spid who runs for cover everytime you prove him wrong.

They will sell this to someone who then creates the coated anode powder. It’s up to the buyer to ensure it meets the qualification standards of the battery manufacturer they are supplying. Lower down the value chain and lower prices.

WheresTheMonkey

Regular

Yeah I get that but isn’t the question whether all mined graphite can be turned into the same quality SPG ?As I understand it, PSG is not the same as Talnode-C. PSG is Purified Spheronised Natural Graphite. It still needs to be coated to produce the battery ready coated anode powder i.e active anode material.

They will sell this to someone who then creates the coated anode powder. It’s up to the buyer to ensure it meets the qualification standards of the battery manufacturer they are supplying. Lower down the value chain and lower prices.

Therefore a new qualification for OEMs

Ecograf is pulling stuff from anywhere they can get it

Ok shit product works for mobile phones, your little Bose speaker, your recreational drone that you will crash in 3 years

Short term stuff

But it won’t work for an OEM doing EVs that need to last 10 plus years

I don’t get the business model

Remember MT said he is careful about who he wants to do offtakes with ?

Microns microns microns it’s all about …….

Size counts ………… for an OEM

Slymeat

Move on, nothing to see.

Geo-based fingerprinting has some interesting developments and may actually be able to help prove/disprove traceability of all EV materials.

A major concern with traceability of environmental impact is that it is open to corruption. Who would have ever thought that! Maybe geo-based fingerprinting can be developed to a suitable degree to help at least prove or disprove this. It could be handy for rejecting material from known problem spots that have practices that don’t consider human rights or/and the environment.

This will stop processors buying the cheapest shit on the market and flogging it off as socially and environmentally friendly.

Conversely, any company that develops appropriate processes (world-wide applicable, in real time, and at a reasonable cost) to perform geo-based fingerprinting, may be worth investing in. I expect the start-up costs of developing, and maintaining, a world-wide database may be high, as well as difficult to get for the countries it will most likely target. A simple solution is to instantly declare as unusable, products from any country that isn‘t open.

It is one thing to ask a company to provide figures on environmental and human rights impact. It is next step, and better IMHO, to have a process that can audit that the supplied facts are at least believable.

A major concern with traceability of environmental impact is that it is open to corruption. Who would have ever thought that! Maybe geo-based fingerprinting can be developed to a suitable degree to help at least prove or disprove this. It could be handy for rejecting material from known problem spots that have practices that don’t consider human rights or/and the environment.

This will stop processors buying the cheapest shit on the market and flogging it off as socially and environmentally friendly.

Conversely, any company that develops appropriate processes (world-wide applicable, in real time, and at a reasonable cost) to perform geo-based fingerprinting, may be worth investing in. I expect the start-up costs of developing, and maintaining, a world-wide database may be high, as well as difficult to get for the countries it will most likely target. A simple solution is to instantly declare as unusable, products from any country that isn‘t open.

It is one thing to ask a company to provide figures on environmental and human rights impact. It is next step, and better IMHO, to have a process that can audit that the supplied facts are at least believable.

catdog

Member

Nope, not all graphite can be turned into the same PSG. The graphite source and it’s characteristics determines the quality, the application and price, or how it is mixed with synthetic anode. Ecograf PSG may meet the qualification standards for certain lower end batteries so is fine, or is mixed with synthetic anode to meet the qualification standards of the end customer. This is the current process of Chinese anode suppliers, they mix poor quality natural graphite anode from multiple sources with synthetic anode to meet the customer requirements. MT mentioned this in the recent webinar as the traditional misconception with natural graphite not being as good as synthetic anode. It’s all about the graphite.Yeah I get that but isn’t the question whether all mined graphite can be turned into the same quality SPG ?

Therefore a new qualification for OEMs

Ecograf is pulling stuff from anywhere they can get it

Ok shit product works for mobile phones, your little Bose speaker, your recreational drone that you will crash in 3 years

Short term stuff

But it won’t work for an OEM doing EVs that need to last 10 plus years

I don’t get the business model

Remember MT said he is careful about who he wants to do offtakes with ?

Microns microns microns it’s all about …….

Size counts ………… for an OEM

Talga are trying to achieve a complete synthetic anode replacement with natural graphite, which is novel to current practices, and is due to the the unique nature of the Vittangi graphite. This achieves higher prices and performance than typical natural graphite and I’m sure is subject to strict qualification to prove it does actually meet the standard on a commercial scale.

I think this is the point, what Talga are doing, due to the unique recourse is new to the battery industry.

catdog

Member

You have to remember MT is a well respected geologist in Australia and doesn’t call himself the dinosaur man for nothing. Check his early webinars and he said he scoured the world looking at all the graphite resources and decided on Vittangi because it was a freak of nature thanks to the Cyanobacteria. Other graphite resources simply can’t match the quality of Vittangi graphite.Nope, not all graphite can be turned into the same PSG. The graphite source and it’s characteristics determines the quality, the application and price, or how it is mixed with synthetic anode. Ecograf PSG may meet the qualification standards for certain lower end batteries so is fine, or is mixed with synthetic anode to meet the qualification standards of the end customer. This is the current process of Chinese anode suppliers, they mix poor quality natural graphite anode from multiple sources with synthetic anode to meet the customer requirements. MT mentioned this in the recent webinar as the traditional misconception with natural graphite not being as good as synthetic anode. It’s all about the graphite.

Talga are trying to achieve a complete synthetic anode replacement with natural graphite, which is novel to current practices, and is due to the the unique nature of the Vittangi graphite. This achieves higher prices and performance than typical natural graphite and I’m sure is subject to strict qualification to prove it does actually meet the standard on a commercial scale.

I think this is the point, what Talga are doing, due to the unique recourse is new to the battery industry.

catdog

Member

Fun fact - Mark is also a world renowned palaeontologist.You have to remember MT is a well respected geologist in Australia and doesn’t call himself the dinosaur man for nothing. Check his early webinars and he said he scoured the world looking at all the graphite resources and decided on Vittangi because it was a freak of nature thanks to the Cyanobacteria. Other graphite resources simply can’t match the quality of Vittangi graphite.

He discovered one of the most important dinosaur fossils in a century with a Guinness world record for the best preserved dinosaur. He was then embroiled in a scandal as one of his colleagues tried to steal the fossil.

Mark Thompson discovered a dinosaur

ABC Rural News provides authoritative coverage of the business and politics of Australian farming, livestock, forestry, agriculture and primary production

Perfectly preserved dinosaur stuns palaeontologists

THE discovery of a dinosaur "mummy", complete with stomach contents, promises to be one of the most important dinosaur discoveries for years. The remains should reveal new details about the dinosaur's diet, as well as its muscles, movement and development. The dinosaur, a young plant-eating...

MARK THOMPSON at THE WESTERN AUSTRALIAN NATURALISTS' CLUB - Sydney Mineral Exploration Discussion Group

THE WESTERN AUSTRALIAN NATURALISTS’ CLUB Presents AN ILLUSTRATED PUBLIC TALK ON DINOSAUR DISCOVERIES by Mark Thompson A DINOSAUR TALE: DISCOVERING MONTANA’S NATURAL TREASURES Mark was a team leader for the discovery of ‘Leonardo’, a complete and incredible preserved duckbill dinosaur that...

MARK THOMPSON at THE WESTERN AUSTRALIAN NATURALISTS' CLUB - Sydney Mineral Exploration Discussion Group

THE WESTERN AUSTRALIAN NATURALISTS’ CLUB Presents AN ILLUSTRATED PUBLIC TALK ON DINOSAUR DISCOVERIES by Mark Thompson A DINOSAUR TALE: DISCOVERING MONTANA’S NATURAL TREASURES Mark was a team leader for the discovery of ‘Leonardo’, a complete and incredible preserved duckbill dinosaur that...

Instead of Glory, the Finder of a Rare Dinosaur Fossil Faces Charges of Theft

A respected amateur paleontologist in Montana has been charged with theft after investigators said he took a rare dinosaur fossil from land he was not authorized to excavate.

www.tuscaloosanews.com

cosors

👀

Thanks for your explanations! You are absolutely right that he is a respected geologist and knows exactly what he is doing. And for the others who don't know the company for so long:You have to remember MT is a well respected geologist in Australia and doesn’t call himself the dinosaur man for nothing. Check his early webinars and he said he scoured the world looking at all the graphite resources and decided on Vittangi because it was a freak of nature thanks to the Cyanobacteria. Other graphite resources simply can’t match the quality of Vittangi graphite.

"INSIGHTS FROM INDUSTRY

Developing the World’s First Industrial Graphene Supply

Interview conducted by Alexander ChiltonJul 30 2015

Mark Thompson, Managing Director of Talga Resources Limited, talks to AZoNano about their unique, simple and cost effective process to liberate graphene directly from its large high quality graphite ore deposits.

Could you provide our readers with an overview of Talga Resources Limited and explain how the company has changed since it floated on the Australian Securities Exchange (ASX) back in 2010?

We started off as a gold focused company and we recognised the graphite space becoming of more and more economic importance in 2011.We secured our graphite projects in Sweden in 2012 and it was during the development of our flagship project at Vittangi that we discovered that both graphite and graphene could be liberated from the ore in a rather special way in early 2014.

That leads us nicely to where we are today in 2015. We celebrated our 5th year anniversary last month, with the company having a market value of approximately 7 times of when it started.

Mark, you personally entered the graphene processing industry from a geological background, having spent more than 20 years working on mineral exploration and mining management. How has your previous experience influenced the way in which Talga views the graphene processing market and the way it operates within it?

Certainly as graphene is a material that has been largely difficult to manufacture and is still developing in its market, it means that it is an industry which is weighted towards more scientific knowledge when it comes to the management and development of graphene companies. I think my experience in a geology and mineral career has allowed me to have a more complete view of the material process from the mine to the market.

I find that many people in the graphene sector from the academic side did not understand where the graphite precursors came from depending on how they were making their graphene. If they were making it from a natural graphite source I found that they did not understand the quantity of steps, the expense and the environmental footprint of their graphite supply before they’d even begun to commence a graphene production process.

Coming from the other side of it, it allows you to develop an objective view of natural advantages through the whole process from the first cost and the natural abundance of materials through to the way that feeds into the economic side of graphene production. I have found this an advantage to date.

Why is it very important to carefully consider the source material you use when producing and processing graphene? What are the advantages of doing so in terms of the cost of the production process and the quality of the end material?

There are fundamentals such as crystallinity and grain size that can feed into any resulting graphene process but I find mostly that if you consider carefully the source material, then that sets up the economic conditions for the graphene production process.For example, if you look at what has happened in the lithium production market. For many years the way we produced lithium was from hard rock sources and there has been in more recent years a greater focus on saline sources of lithium. This is much more economic as a source of lithium than hard rock, so the source supply of that material changes your economic costs and your margins when producing it.

If you can source a graphitic precursor that has got as big a benefit as, say liquid versus hard rock, or in our case things like crush and grind versus another method which liberates the graphene, you see that an economic condition that is more advantageous than other pathways. That is why the source of the material is really the start of solving the problems that there has been in graphene production.

What do you believe sets Talga Resources apart from pure play graphene companies and gives you a true competitive advantage within the graphene market?

The main advantage is probably volume – as we make graphene almost as a by-product of our graphite mining, we can produce graphene on a scale than is more akin to graphite mining. By comparison to pure play start-ups, it is the sheer volume because we mine our source material, we are developing our source material and processing it in a way to suit another market – the graphene as I mentioned is almost like a by-product.This allows us to produce massive volumes compared to what other companies can produce so it’s scalable and also means the cost basis is much lower than other routes. Also, fundamentally as a business model, the company can make money from its graphite assets as well as its gold, cobalt and other assets so Talga does not live or die by whether the graphene market commercialises or not at the speed which we hope it will.

The business model of the company runs very profitably on the standard industrial commodity supply of graphite and therefore we are not actually reliant on the commercialisation of the graphene market to make money, it just means that we will make more money if the market grows in the way in which we believe it will.

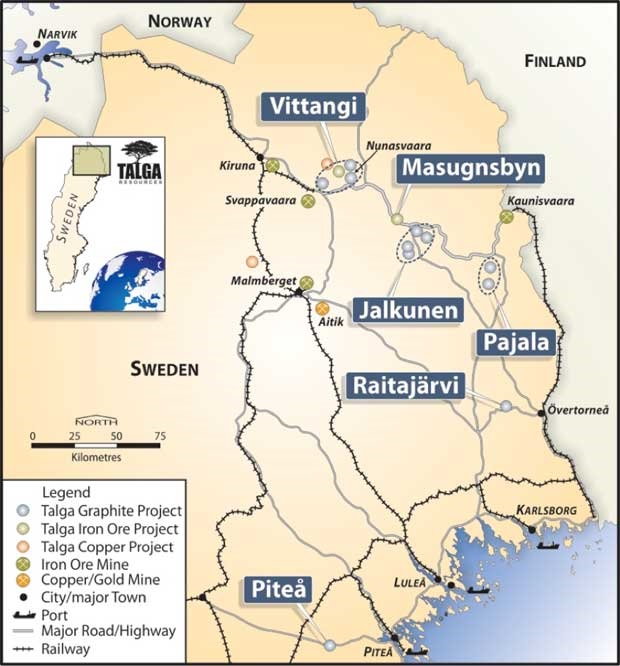

Talga Resources now has five 100% owned graphite projects in Sweden. Could you explain to our readers where these projects are geographically within Sweden and how the deposits vary by location?

All the deposits are in the north of Sweden, mainly in the Norrbotten district, which is one of the largest mining producing areas of the country. It has been the home of some of Europe’s largest iron ore, copper and gold mines for nearly one thousand years so it is clearly an area of Sweden with an active mining district.

The deposits range from the highest grade technical resource in the world at nearly 25% at the Vittangi project to deposits which have resources down to 7% graphitic carbon grade ranges. The deposits at the five projects cover a complete range of sizes from less than 75 microns to 80% of them being bigger than 300 microns in size.

Probably more importantly, the particular process we use in an advantageous way to get the graphene and the graphite supply from the rock only covers two of the five projects. We have standard slate-graphite projects which can be developed into materials that would suit the full range of graphite specifications. Two particular projects are exceptionally high grade and they have been proven to liberate graphene as well as graphite in a unique, low cost and scalable way.

Last month (26th June 2015) Talga Resources announced the commencement of site works in relation to its trial mining program at the Vittangi graphite project. Could you summarise the latest developments on this project to our readers?

Related Stories

We made a decision around 6 months ago, as part of the development towards a full scale mine in Sweden which would take between 2 and 3 years, that in the meantime we would undertake some trial mining at the Vittangi project to prove the methodology we propose and that we can therefore treat larger amounts of material through this process. This will allow us to not only prove what is a world first in the mining to processing method but allows us to confirm that this method can be scaled up to full scale production.It has also provided the opportunity to gain large channels of graphene to supply to the market where companies and products which we have identified with large volumes need quite large sample sizes to accelerate the development of the product. That is why we are undertaking trial mining as well as pilot plant processing in Germany so that we can advance the market faster.

Talga Resources recently secured a site in central Germany for a demonstration plant to process your high-grade graphite ore from your deposits in Sweden. Why did you decide to construct a pilot plant there rather than in Sweden? What are the advantages of choosing this location?

There are many advantages to being based in both countries. We chose the deposits in Sweden because they are exceptional deposits and quite unique in the world in the way they work and their exceptionally high grade. Sweden has also got very advantageous tax and mining laws. The infrastructure and low cost power in Sweden is really second to none anywhere in the world.It really is a great place to be developing and producing our precursor graphite material but we also recognise that north Sweden is quite far away from end users who may be in Europe and the analytics which are required in order to work with quite high precision graphene.

We have several research programs running on the graphene production process and utilising graphene in products in central Germany. There was a real speed benefit as there were government buildings available to lease which we could turn into a pilot plant. There are also quite generous research and development concessions from the local government.

It was faster and cheaper to build the pilot processing plant in Germany and transport the material down from Sweden than to construct all of those facilities in north Sweden in the time frame we wanted. The time frame we are talking about here was 4 months – we have got to the stage we are at now in 4 months from the decision to do it so it needed to be very rapid by going to the Thuringia area of Germany.

An additional benefit is that the research programs give us access to world class analytical facilities for the characterisation of the material and the integration of the graphene into customer’s products, which means that it can happen a lot faster. It also provides a facility where end users can see what we are doing and get some comfort from the fact that we have a consistent high-quality process and a real industrial example of graphene production rather than something theoretical.

When do you believe the pilot plant in Germany will be operating at full scale? Will this remain your main processing plant or do you have plans to move to an alternative location in the long term?

The German pilot plant will be scaling itself up through several phases until it is at full scale in 2016. It will be our primary processing plant for approximately two years until our site in Sweden is ready to go into full scale production and then everything will shift to Sweden.The German plant is expected to continue to operate in some sort of R&D or even small retail type way but the bulk of production will shift to Sweden and the material will be processed on site. In the meantime, it is certainly cheaper and faster to do it in this way.

What are the main markets and application areas which you are targeting with the graphene you produce?

Because of our potential for volume, we are focusing on graphene as an additive. Within that sphere are things like composites, 3D printing inks, conductive inks, paints, anti-corrosion coatings, galvanic applications on to steel, plastics and polymers such PET material or packaging material.We are focussing mainly on the additive applications which have not only large volume but also good margins and are current products. We do not require new products to be created which do not exist yet, we just looking at making current products better.

We see this as the fastest pathway for graphene to commercialise and its one that we feel is a lot better developed behind the scenes than the media has been picking up on because there is a focus on well-hyped futuristic applications of graphene rather than the fundamentals of how it can affect every day materials.

What do you believe is the biggest challenge which the graphene industry has to overcome before this 'wonder material' can be fully commercialised in the near future?

I differ from a lot of people in industry at this point who keep seeking a killer application. I actually think that to just focus on one single graphene only application is a little furphy. I have seen many trial products that have not been able to continue onto production because of the lack of volume in the supply of graphene and the associated high costs of the material.I see volume and costs as the chicken to graphene’s egg. Most people have been waiting for graphene but they have not solved the volume or the cost problem. When you solve these problems then you can enable all sorts of graphene applications to occur and a couple of those might turn out to be killer applications. I see the production side as being the main hold-up.

When you have a material like graphene with extraordinary properties such as strength, conductivity, transparency in some applications amongst others, and it seems that there is quite an abundance of evidence in how it can affect everyday materials then you do not need a killer application, you just need to solve the supply problem.

Where can our readers find out more information about Talga Resources?

Our website also has details of our company including presentations and the latest news: http://www.talgaresources.com/IRM/content/default.aspxYou can also meet us at the graphene and technology conferences where you should review who else is talking about solving the main problem of graphene supply.

Look at what the other companies are not yet solving and are not yet producing for some information about where Talga is going in the future.

About Mark Thompson

Mark Thompson has more than 20 years industry experience in mineral exploration and mining management, working extensively on major resource projects throughout Australia, Africa and South America.He is a member of the Australian Institute of Geoscientists and the Society of Economic Geologists, and holds the position of Guest Professor in Mineral Exploration Technology at both the Chengdu University of Technology and the Southwest University of Science and Technology in China. Mark Thompson founded and served on the Board of ASX listed Catalyst Metals Ltd and is a Non-Executive Director of Phosphate Australia Ltd."

https://www.azonano.com/article.aspx?ArticleID=4109

cosors

👀

Thank you again, this is very interesting!Fun fact - Mark is also a world renowned palaeontologist.

He discovered one of the most important dinosaur fossils in a century with a Guinness world record for the best preserved dinosaur. He was then embroiled in a scandal as one of his colleagues tried to steal the fossil.

Mark Thompson discovered a dinosaur

ABC Rural News provides authoritative coverage of the business and politics of Australian farming, livestock, forestry, agriculture and primary productionwww.abc.net.au

Perfectly preserved dinosaur stuns palaeontologists

THE discovery of a dinosaur "mummy", complete with stomach contents, promises to be one of the most important dinosaur discoveries for years. The remains should reveal new details about the dinosaur's diet, as well as its muscles, movement and development. The dinosaur, a young plant-eating...www.newscientist.com

MARK THOMPSON at THE WESTERN AUSTRALIAN NATURALISTS' CLUB - Sydney Mineral Exploration Discussion Group

THE WESTERN AUSTRALIAN NATURALISTS’ CLUB Presents AN ILLUSTRATED PUBLIC TALK ON DINOSAUR DISCOVERIES by Mark Thompson A DINOSAUR TALE: DISCOVERING MONTANA’S NATURAL TREASURES Mark was a team leader for the discovery of ‘Leonardo’, a complete and incredible preserved duckbill dinosaur that...smedg.org.au

MARK THOMPSON at THE WESTERN AUSTRALIAN NATURALISTS' CLUB - Sydney Mineral Exploration Discussion Group

THE WESTERN AUSTRALIAN NATURALISTS’ CLUB Presents AN ILLUSTRATED PUBLIC TALK ON DINOSAUR DISCOVERIES by Mark Thompson A DINOSAUR TALE: DISCOVERING MONTANA’S NATURAL TREASURES Mark was a team leader for the discovery of ‘Leonardo’, a complete and incredible preserved duckbill dinosaur that...

Instead of Glory, the Finder of a Rare Dinosaur Fossil Faces Charges of Theft

A respected amateur paleontologist in Montana has been charged with theft after investigators said he took a rare dinosaur fossil from land he was not authorized to excavate.www.tuscaloosanews.com

I think it's about time that MT is appreciated a little here. In this new place we have mainly licked the wounds and perhaps the big and whole or MT's work too little appreciated. We now catch up thanks to you @catdog !

I see that his dinosaur find was so great that it immediately became a major project with great promotion. Unfortunately, others have then apparently very quickly profiled and pushed in front of him

Who is still interested in MT dinosaur find Leonardo more precisely:

http://www.dinosaurmummy.org/the-discovery.html The page seems to have been created because of his find.

And here a detailed insight:

https://www.cgw.com/Publications/CGW/2009/Volume-32-Issue-7-July-2009-/Dino-Might.aspx

And believe it or not the pictures from the article make me recognize Leonardo or MTs Dinosaur. I've seen him in documentaries before. It's a small world! Who would have thought that MT is responsible for this!

Last edited:

So Talga graphite is superior to all other graphite in quality and performance. But where is the independent proof of this?You have to remember MT is a well respected geologist in Australia and doesn’t call himself the dinosaur man for nothing. Check his early webinars and he said he scoured the world looking at all the graphite resources and decided on Vittangi because it was a freak of nature thanks to the Cyanobacteria. Other graphite resources simply can’t match the quality of Vittangi graphite.

Its time to see the results from outside testing., Not just taking MT at his word. MT needs to justify the top end price of Talga graphite.

Slymeat

Move on, nothing to see.

Thanks @cosors for this very interesting, and now historical, article. It highlights the original reason why I invested in Talga—back then Graphene Was far more prominent in their considerations. But I accept that now being a byproduct. The world is yet to catch on to the benefits Graphene has to offer and Is hungry for batteries, and hence graphite.Thanks for your explanations! You are absolutely right that he is a respected geologist and knows exactly what he is doing. And for the others who don't know the company for so long:

"INSIGHTS FROM INDUSTRY

Developing the World’s First Industrial Graphene Supply

Interview conducted by Alexander ChiltonJul 30 2015

Mark Thompson, Managing Director of Talga Resources Limited, talks to AZoNano about their unique, simple and cost effective process to liberate graphene directly from its large high quality graphite ore deposits.

Could you provide our readers with an overview of Talga Resources Limited and explain how the company has changed since it floated on the Australian Securities Exchange (ASX) back in 2010?

We started off as a gold focused company and we recognised the graphite space becoming of more and more economic importance in 2011.

We secured our graphite projects in Sweden in 2012 and it was during the development of our flagship project at Vittangi that we discovered that both graphite and graphene could be liberated from the ore in a rather special way in early 2014.

That leads us nicely to where we are today in 2015. We celebrated our 5th year anniversary last month, with the company having a market value of approximately 7 times of when it started.

Mark, you personally entered the graphene processing industry from a geological background, having spent more than 20 years working on mineral exploration and mining management. How has your previous experience influenced the way in which Talga views the graphene processing market and the way it operates within it?

Certainly as graphene is a material that has been largely difficult to manufacture and is still developing in its market, it means that it is an industry which is weighted towards more scientific knowledge when it comes to the management and development of graphene companies. I think my experience in a geology and mineral career has allowed me to have a more complete view of the material process from the mine to the market.

I find that many people in the graphene sector from the academic side did not understand where the graphite precursors came from depending on how they were making their graphene. If they were making it from a natural graphite source I found that they did not understand the quantity of steps, the expense and the environmental footprint of their graphite supply before they’d even begun to commence a graphene production process.

Coming from the other side of it, it allows you to develop an objective view of natural advantages through the whole process from the first cost and the natural abundance of materials through to the way that feeds into the economic side of graphene production. I have found this an advantage to date.

Why is it very important to carefully consider the source material you use when producing and processing graphene? What are the advantages of doing so in terms of the cost of the production process and the quality of the end material?

There are fundamentals such as crystallinity and grain size that can feed into any resulting graphene process but I find mostly that if you consider carefully the source material, then that sets up the economic conditions for the graphene production process.

For example, if you look at what has happened in the lithium production market. For many years the way we produced lithium was from hard rock sources and there has been in more recent years a greater focus on saline sources of lithium. This is much more economic as a source of lithium than hard rock, so the source supply of that material changes your economic costs and your margins when producing it.

If you can source a graphitic precursor that has got as big a benefit as, say liquid versus hard rock, or in our case things like crush and grind versus another method which liberates the graphene, you see that an economic condition that is more advantageous than other pathways. That is why the source of the material is really the start of solving the problems that there has been in graphene production.

What do you believe sets Talga Resources apart from pure play graphene companies and gives you a true competitive advantage within the graphene market?

The main advantage is probably volume – as we make graphene almost as a by-product of our graphite mining, we can produce graphene on a scale than is more akin to graphite mining. By comparison to pure play start-ups, it is the sheer volume because we mine our source material, we are developing our source material and processing it in a way to suit another market – the graphene as I mentioned is almost like a by-product.

This allows us to produce massive volumes compared to what other companies can produce so it’s scalable and also means the cost basis is much lower than other routes. Also, fundamentally as a business model, the company can make money from its graphite assets as well as its gold, cobalt and other assets so Talga does not live or die by whether the graphene market commercialises or not at the speed which we hope it will.

The business model of the company runs very profitably on the standard industrial commodity supply of graphite and therefore we are not actually reliant on the commercialisation of the graphene market to make money, it just means that we will make more money if the market grows in the way in which we believe it will.

Talga Resources now has five 100% owned graphite projects in Sweden. Could you explain to our readers where these projects are geographically within Sweden and how the deposits vary by location?

All the deposits are in the north of Sweden, mainly in the Norrbotten district, which is one of the largest mining producing areas of the country. It has been the home of some of Europe’s largest iron ore, copper and gold mines for nearly one thousand years so it is clearly an area of Sweden with an active mining district.

The deposits range from the highest grade technical resource in the world at nearly 25% at the Vittangi project to deposits which have resources down to 7% graphitic carbon grade ranges. The deposits at the five projects cover a complete range of sizes from less than 75 microns to 80% of them being bigger than 300 microns in size.

Probably more importantly, the particular process we use in an advantageous way to get the graphene and the graphite supply from the rock only covers two of the five projects. We have standard slate-graphite projects which can be developed into materials that would suit the full range of graphite specifications. Two particular projects are exceptionally high grade and they have been proven to liberate graphene as well as graphite in a unique, low cost and scalable way.

Last month (26th June 2015) Talga Resources announced the commencement of site works in relation to its trial mining program at the Vittangi graphite project. Could you summarise the latest developments on this project to our readers?

Related Stories

We made a decision around 6 months ago, as part of the development towards a full scale mine in Sweden which would take between 2 and 3 years, that in the meantime we would undertake some trial mining at the Vittangi project to prove the methodology we propose and that we can therefore treat larger amounts of material through this process. This will allow us to not only prove what is a world first in the mining to processing method but allows us to confirm that this method can be scaled up to full scale production.

It has also provided the opportunity to gain large channels of graphene to supply to the market where companies and products which we have identified with large volumes need quite large sample sizes to accelerate the development of the product. That is why we are undertaking trial mining as well as pilot plant processing in Germany so that we can advance the market faster.

Talga Resources recently secured a site in central Germany for a demonstration plant to process your high-grade graphite ore from your deposits in Sweden. Why did you decide to construct a pilot plant there rather than in Sweden? What are the advantages of choosing this location?

There are many advantages to being based in both countries. We chose the deposits in Sweden because they are exceptional deposits and quite unique in the world in the way they work and their exceptionally high grade. Sweden has also got very advantageous tax and mining laws. The infrastructure and low cost power in Sweden is really second to none anywhere in the world.

It really is a great place to be developing and producing our precursor graphite material but we also recognise that north Sweden is quite far away from end users who may be in Europe and the analytics which are required in order to work with quite high precision graphene.

We have several research programs running on the graphene production process and utilising graphene in products in central Germany. There was a real speed benefit as there were government buildings available to lease which we could turn into a pilot plant. There are also quite generous research and development concessions from the local government.

It was faster and cheaper to build the pilot processing plant in Germany and transport the material down from Sweden than to construct all of those facilities in north Sweden in the time frame we wanted. The time frame we are talking about here was 4 months – we have got to the stage we are at now in 4 months from the decision to do it so it needed to be very rapid by going to the Thuringia area of Germany.

An additional benefit is that the research programs give us access to world class analytical facilities for the characterisation of the material and the integration of the graphene into customer’s products, which means that it can happen a lot faster. It also provides a facility where end users can see what we are doing and get some comfort from the fact that we have a consistent high-quality process and a real industrial example of graphene production rather than something theoretical.

When do you believe the pilot plant in Germany will be operating at full scale? Will this remain your main processing plant or do you have plans to move to an alternative location in the long term?

The German pilot plant will be scaling itself up through several phases until it is at full scale in 2016. It will be our primary processing plant for approximately two years until our site in Sweden is ready to go into full scale production and then everything will shift to Sweden.

The German plant is expected to continue to operate in some sort of R&D or even small retail type way but the bulk of production will shift to Sweden and the material will be processed on site. In the meantime, it is certainly cheaper and faster to do it in this way.

What are the main markets and application areas which you are targeting with the graphene you produce?

Because of our potential for volume, we are focusing on graphene as an additive. Within that sphere are things like composites, 3D printing inks, conductive inks, paints, anti-corrosion coatings, galvanic applications on to steel, plastics and polymers such PET material or packaging material.

We are focussing mainly on the additive applications which have not only large volume but also good margins and are current products. We do not require new products to be created which do not exist yet, we just looking at making current products better.

We see this as the fastest pathway for graphene to commercialise and its one that we feel is a lot better developed behind the scenes than the media has been picking up on because there is a focus on well-hyped futuristic applications of graphene rather than the fundamentals of how it can affect every day materials.

What do you believe is the biggest challenge which the graphene industry has to overcome before this 'wonder material' can be fully commercialised in the near future?

I differ from a lot of people in industry at this point who keep seeking a killer application. I actually think that to just focus on one single graphene only application is a little furphy. I have seen many trial products that have not been able to continue onto production because of the lack of volume in the supply of graphene and the associated high costs of the material.

I see volume and costs as the chicken to graphene’s egg. Most people have been waiting for graphene but they have not solved the volume or the cost problem. When you solve these problems then you can enable all sorts of graphene applications to occur and a couple of those might turn out to be killer applications. I see the production side as being the main hold-up.

When you have a material like graphene with extraordinary properties such as strength, conductivity, transparency in some applications amongst others, and it seems that there is quite an abundance of evidence in how it can affect everyday materials then you do not need a killer application, you just need to solve the supply problem.

Where can our readers find out more information about Talga Resources?

Our website also has details of our company including presentations and the latest news: http://www.talgaresources.com/IRM/content/default.aspx

You can also meet us at the graphene and technology conferences where you should review who else is talking about solving the main problem of graphene supply.

Look at what the other companies are not yet solving and are not yet producing for some information about where Talga is going in the future.

About Mark Thompson

Mark Thompson has more than 20 years industry experience in mineral exploration and mining management, working extensively on major resource projects throughout Australia, Africa and South America.

He is a member of the Australian Institute of Geoscientists and the Society of Economic Geologists, and holds the position of Guest Professor in Mineral Exploration Technology at both the Chengdu University of Technology and the Southwest University of Science and Technology in China. Mark Thompson founded and served on the Board of ASX listed Catalyst Metals Ltd and is a Non-Executive Director of Phosphate Australia Ltd."

https://www.azonano.com/article.aspx?ArticleID=4109

Graphene’s time will come!

You can see just how pragmatic and ‘real world’ focussed he was back then about there was no need for graphene to develop a new unique super product to be viable, what is instead lacking is the volume to add to exisiting products to make them better.Thanks @cosors for this very interesting, and now historical, article. It highlights the original reason why I invested in Talga—back then Graphene Was far more prominent in their considerations. But I accept that now being a byproduct. The world is yet to catch on to the benefits Graphene has to offer and Is hungry for batteries, and hence graphite.

Graphene’s time will come!

I think you will get your wish on the graphene side with all that R&D work into the space - once Talga have the volume available at a more competitive price point than available now, suddenly the binding offtakes will appear!

Similar threads

- Replies

- 18

- Views

- 4K

- Replies

- 6

- Views

- 3K

- Article

- Replies

- 13

- Views

- 5K

- Replies

- 2

- Views

- 2K