cosors

👀

"25 March 2025

SGU welcomes Swedish strategic projects in the mineral sector

Today, 25 March, the European Commission has announced its strategic projects under the Critical Raw Materials Regulation. Among the selected projects are five Swedish projects that aim to increase Sweden's security of supply and create stable value chains for critical metals and minerals. The Geological Survey of Sweden (SGU) welcomes the decision.The first list of strategic projects under the EU Critical Raw Materials Act has been published by the European Commission at a press conference today. Of the 170 applications for strategic projects received by the Commission during the first application period, 47 projects have been selected. The list includes five Swedish projects, three of which are sub-projects within the same company:

- LKAB's ReeMAP Project, which consists of three sub-projects: extraction of rare earths and phosphorus in Malmberget, recycling of critical raw materials from mining waste in Luleå, and extraction of rare earths in the Per Geijer deposit in Kiruna

- Northvolt Revolt AB, for the recovery of the battery metals manganese, lithium, graphite, nickel and cobalt

- Talga Natural Graphite ONE, for the extraction of graphite

- ‘It is gratifying that these Swedish projects will now have the opportunity for a faster and clearer authorisation process. SGU would like to congratulate these companies, which are so important for both Sweden's and Europe's security of supply. But I would also like to take this opportunity to say that the projects that have not been selected this time are of great importance for the Swedish minerals industry,’ says Anette Madsen, Director General of SGU.

The projects selected have been assessed on the basis of a number of different criteria. The selection aims to reflect the goals set out in the regulation that by 2030 the EU should account for 10 per cent own extraction, 40 per cent own processing and 25 per cent own recycling of raw materials.

- ‘The European Commission seems to have placed great emphasis on the designated projects being able to deliver before 2030. It is also worth noting that great emphasis seems to have been placed on the so-called battery metals,’ says Kaj Lax, acting head of the Department of Mineral Resources at SGU.

SGU is tasked with promoting Sweden as a mining and exploration country. Among other things, this is done by mapping potential ore areas. For example, the levels of rare earth elements in LKAB's Per Geijer deposit, which is now closer than ever to being mined, were identified as early as 1931 by SGU's state geologist Per Geijer.

- Sweden is an important mining nation with thousands of years of experience, a bedrock with good conditions and a transparent environmental permit process. Taking responsibility for Sweden's and the EU's security of supply through increased extraction of, among other things, rare earth elements is fundamental to the green transition and our defence capability. It is unreasonable to replace today's dependence on fossil fuels with a total dependence on extraction and production from countries that in many cases lack the democratic rights and environmental legislation we have here,’ says Director-General Anette Madsen.

FACTS Strategic projects under the Critical Raw Materials Act

Under the EU Critical Raw Materials Regulation, there is the possibility to be recognised as a strategic project involving the extraction, processing or recycling of materials. The purpose of designating strategic projects is to strengthen the Union's supply of strategic raw materials. During the first application period, which ran from 23 May to 22 August 2024, the European Commission received over 170 applications. Each year there will be several application periods under the Regulation. Projects that applied but were not selected this time can apply again.Last reviewed on 25 March 2025"

SGU välkomnar svenska strategiska projekt på mineralområdet

I dag, den 25 mars, har EU-kommissionen tillkännagivit vilka de utser som strategiska projekt inom förordningen om kritiska råmaterial. Bland de utvalda projekten finns fem svenska projekt som syftar till att öka Sveriges försörjningstrygghet och skapa stabila värdekedjor för kritiska metaller...

Five years ago, who among us would have expected that the mining association SGU, of all organisations, would be the only one to emphasise the positive environmental aspects, and not simply ignore this like the environmentalists and climate protesters and our Antis do, raise your hand.)

____________

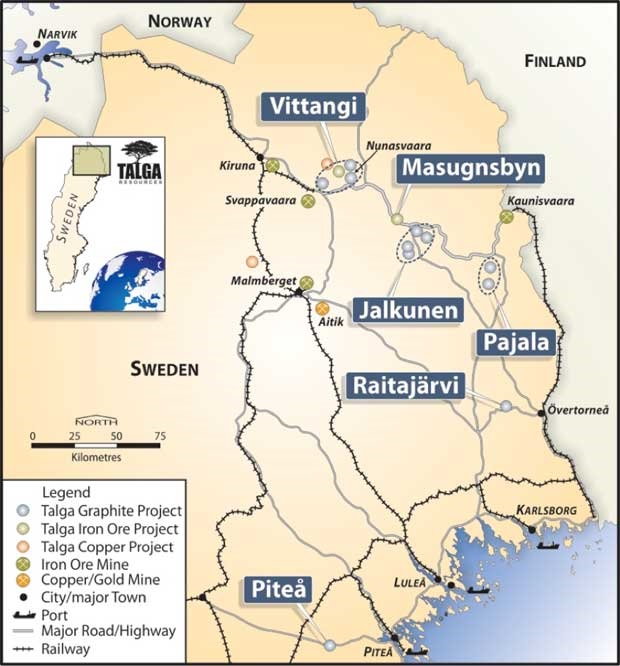

"Mining project gets fast track: ‘Enormous importance’

Five Swedish mining projects are to be fast-tracked after being designated as strategic by the EU, including LKAB's large rare earth deposit in Kiruna and Talga AB's graphite deposit outside Vittangi.- ‘We have tried to exert influence, but it has been rather futile,’ says a critical Matti Blind Berg, chairman of the Swedish Sami National Association.

To make the EU more self-sufficient in critical minerals, the EU adopted a new regulation last year to facilitate the mining industry. Projects listed as strategic will be fast-tracked through the authorisation process, making it easier for companies to get investment. The European Commission has now decided which projects are included. The list of 47 projects includes five Swedish projects, three of which are LKAB's.

- ‘It is of enormous importance that we get metal and minerals to handle the transition required in the future. There will be a shortage that needs to be managed, while we have a geopolitical situation linked to rare earths, which means that China continues to control the entire value chain, which is problematic,’ says Niklas Johansson, LKAB's communications director to Syre.

What do you think it will mean?

- I hope that this will really mean that we can actually get more efficient authorisation processes linked to these projects. I am concerned that we in Sweden risk preserving an unsustainable industrial structure because it is so difficult to move forward.

Sami villages critical

One of LKAB's projects concerns an established iron ore mine where new processes will enable the extraction of rare earth metals and phosphorus from materials that LKAB already mines. The second is an industrial park in Luleå for the processing of phosphorus and rare earths, and the third is the extraction of the large deposit of rare earths in the Per Gejier deposit in Kiruna. The latter project has been heavily criticised, not least by the Gabna Sami village, as it is located on the village's reindeer grazing lands and the mine would block the only remaining migration route for reindeer between winter and summer grazing lands. The Australian company Talga's mine, also designated as a strategic project, is located on the reindeer grazing lands of the Talma Sami community.- ‘A black day for nature,’ village chairman Nils Johanas Allas told DN when the mine was approved by the Land and Environment Court.

‘Have tried to influence’

Matti Blind Berg, chairman of the Swedish Sami Association, is critical of the fact that the organisation has not been invited to a dialogue with the European Commission on the projects that affect the Sami villages' land. A number of environmental organisations have also criticised what they consider to be a lack of transparency in how the projects were selected - and that the rights of indigenous peoples were not taken into account in the selection process.- ‘I have tried to influence, but it has been quite futile. We have not been reached or invited to talks. It's our land*, our territories, our ability to continue to exist as a people. That's what's being jeopardised now,’ says Blind Berg, although he does not attribute any decisive significance to the designation of the mining projects as “strategic”, as they still have to comply with the same legislation.

Do you see any way you could still co-exist with these two projects?

- It might be possible to limit the scope of the projects, but also to ensure that they were run in such a way that they had no impact on the surface. But this will not be the case. It's too economically costly and the technology may not be in place either. So it's a utopia.

‘I think it's difficult’

‘Of course we will need metals and open up new deposits alongside increased recycling,’ says Mr Berg. But this must be done in harmony with the local culture and industries that already exist in these places.- ‘We don't get anywhere near that today, we have mineral legislation that gives all the rights to the mining companies, so it's obvious that we're not there,’ he says.

Niklas Johansson at LKAB is of a different opinion.

- ‘Our ambition must be to find ways forward so that we enable a future for everyone. The best way to do that is through dialogue, talking and finding solutions.

But an invisible mine, something that LKAB previously presented as a possibility and which representatives from the company described as the ‘only solution for mining and reindeer husbandry to coexist’, the company no longer sees as a sustainable technology.

- ‘I think it's difficult,’ says Niklas Johansson."

Detaljplan rivs upp – kan bidra till PFAS-läckage - Syre

Mark- och miljödomstolen upphäver en detaljplan som Karlsborgs kommun antagit, med hänvisning till att kommunen inte tillräckligt utrett hur den kan bidra till PFAS-läckage. – Grundproblemet är att ansvariga för flygplatsen inte tar sitt ansvar, säger Christer Haagman från Aktion rädda Vättern...

tidningensyre.se

tidningensyre.se

*False and a lie. They may use it in 'front of the crown'.

"The reindeer grazing land in Sweden is owned by the state, forestry companies, farmers and other non-Sámi people. The Sámi have extensive usage rights based on ancient traditions."

Last edited:

")