With Gates and Bezos eyeing Congolese lithium, copper explorers making breakthroughs, and Argentina yielding monster deposits, the resource sector is showing serious signs of life

substack.com

AVZ Minerals: A global play attracting global names

Three years after trading suspension and nearly a year since being officially delisted from the ASX,

AVZ Minerals might be on the verge of a breakthrough.

This week may mark the beginning of a long-awaited turnaround for shareholders who've been trapped in limbo since May 2022.

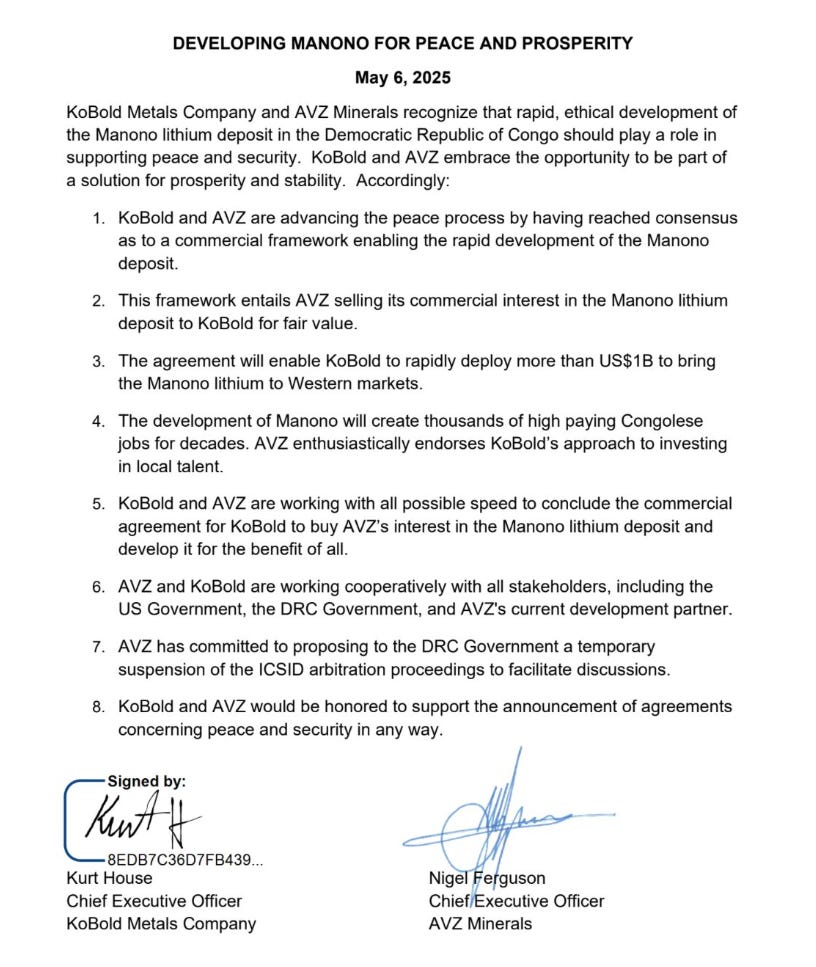

AVZ has now signed a non-binding framework agreement with US-backed Kobold Metals to

purchase its interest in the Manono Lithium and Tin Project in the Democratic Republic of Congo (DRC), the largest undeveloped hard-rock lithium deposit on the planet.

The implications here are big for all involved:

- Kobold Metals is backed by billionaires, including Bill Gates and Jeff Bezos, signalling the strategic relevance of the Manono project on the world stage.

- The US Government recently brokered a peace deal between the DRC and Rwanda, providing a platform for increased investment and regional stability.

- AVZ has publicly endorsed the new agreement and expressed support for US involvement, a sign that the company sees a viable resolution on the horizon.

- The agreement will enable KoBold to potentially deploy more than $US1 billion (AUD$1.55b) to bring the Manono lithium to Western markets.

The deal is designed to resolve the protracted ownership dispute that's plagued the project, with AVZ set to receive compensation for relinquishing its claims and has proposed suspending international arbitration to facilitate the transaction.

Meanwhile, China's Zijin Mining, which was awarded part of the deposit in 2023, would retain control of the northern section while KoBold would develop the southern portion.

AVZ recently secured a US$67.5 million penalty in arbitration against Cominière for ignoring emergency orders in the ongoing dispute.

Framework for KoBold to buy AVZ’s interests in the Manono lithium. Source: Kobold Metals

The company's announcement also made it clear: the window for a constructive, negotiated outcome is open, and AVZ is ready to walk through it.

We've been banging on about AVZ for a while now,

doing a deep dive last year on the immense potential of Manono and the complex dynamics surrounding the project.

AVZ Minerals: From $6 million to a $4.5 billion delisting. Inside the Congo lithium saga

Equities Club

·

May 7, 2024

Read full story

In that piece, we highlighted the asset's strategic position within the lithium supply chain and why it had become the focus of both local political friction and global commercial interest. Today, that thesis is playing out, but now with institutional capital and diplomatic muscle behind it.

So what does this latest update mean for long-suffering shareholders?

The financial terms of the Kobold deal are still being worked out, but signs point to AVZ shareholders finally seeing some return on their patience with it increasingly likely that AVZ could realise meaningful value through a dividend or capital return once the transaction completes.

Manono was never just another lithium deposit. Its sheer size made it a geopolitical chess piece. AVZ shareholders understood this from day one, and those who've white-knuckled through three years of suspension might finally be rewarded for their iron stomachs.

That’s back when AVZ was targeting mining 4.5Mt of ore annually, then they looked at expanding to 10Mt annually so you can take that 100,000 tonnes of LCE annually and more than double it to over 200,000 tonnes of LCE annually

That’s back when AVZ was targeting mining 4.5Mt of ore annually, then they looked at expanding to 10Mt annually so you can take that 100,000 tonnes of LCE annually and more than double it to over 200,000 tonnes of LCE annually")