The Democratic Republic of Congo will have the very first directory of natural resources of soil and subsoil under the supervision of His Excellency Minister of State, Minister of Regional Planning, Mr. Guy LOANDO MBOYO

NATIONAL DIRECTORY OF HYDROCARBON RESOURCES OF THE DEMOCRATIC REPUBLIC OF CONGO

National Directory of Hydrocarbon Resources of the Democratic Republic of Congo

Under the supervision of His Excellency the Minister of State, Minister of Spatial Planning, Mr. Guy LOANDO MBOYO, the Democratic Republic of Congo will have the very first directory of natural resources of the soil and subsoil

Indeed, this Friday, December 16, 2022 was devoted to the closure of the work of the thematic group entitled hydrocarbon resources, in the presence of Councillor Franck MALALE, Rapporteur of the Technical Body of the Multisectoral Committee for the development of the national directory of natural resources of the soil and subsoil of the DRC.

This work, which is part of the Congolese government's project to establish a national directory of renewable and non-renewable natural resources of the soil and subsoil of the Democratic Republic of Congo, has had the participation of several experts operating in different natural resource sectors

With regard to hydrocarbons, experts and representatives of the Ministry of Spatial Planning, the Ministry of Hydrocarbons, SONAHYDROC and the scientific staff of the Faculty of Oil and Gas of the University of Kinshasa formed the thematic group entitled hydrocarbon resources, whose mission was to present the hydrocarbon resources of the Democratic Republic of Congo, both upstream and downstream.

The work of this thematic group, led jointly by Mr. GUSTAVE NGALAMULUME, Director and Head of department in the exploration-production, petrochemical and refining department of the General Secretariat for hydrocarbons and teacher at the Faculty of Oil and Gas of the University of Kinshasa as well as Mr. Kevin ESHIMATA NGIMBI Legal Advisor in the office of the Minister of State hydrocarbons carried by these areas as well as many other aspects surrounding this sector.

In addition, these experts also presented the roles of each institutional actor and operators in the sector, without failing to address the various common issues encountered in the management of the said sector in the DRC.

It should be noted that they have also highlighted the various institutional and legal tools available to the Congolese State, which continues to include its efforts in the establishment and strengthening of mechanisms that prove a healthier and more effective management of the sector.

During the work of this thematic group, the experts also took care to develop the axes that make up the country's hydrocarbon policy as defined by the government's action program, because through upstream and downstream activities, hydrocarbons are likely to play a significant role in the country's economy. They alone can provide the country with the financial resources necessary for the materialization of all development projects.

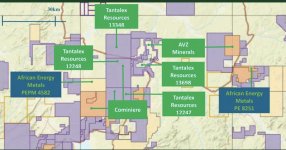

This directory, which will be made available to the public in the near future, also includes newly developed maps, for a better illustration and to allow all those interested in the hydrocarbon sector to understand the issues surrounding it

It's coming Sita

).

).