CashKing

Regular

Pointy end again mate.Is it just me or is getting snarky in here?

Always does

Pointy end again mate.Is it just me or is getting snarky in here?

"US closes in on critical minerals deal with DR Congo"

- Orion Resource Partners

- Robert Friedland

- Rio Tinto

- United Mining

Published April 6 2025

US closes in on critical minerals deal with DR Congo

There is no 'current share price' ...

You don't have to apologise.Ah apologies cruiser but where did I post that i didn’t know what I was posting?

I think you may have missed that my post blaming the nut was a joke!

And yes I posted a meme of trump and Putin dressed as gimps. Which obviously was offensive to a few. Sorry all those offended by it.

Zeebot removed said offensive meme and I take full ownership of it as well.

One thing I’ll never do however is personally attack other posters as I have a lot of respect for a lot of the posters here like you, spike and especially the Winenut!

Thanks

LOL What a total crock of shit.

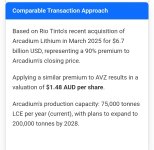

In other words, they've done whatever they could to produce the lowest number possible while trying to present a veneer of authenticity.Lots of factors missing in that valuation. It looks like some high school homework.

For starters, strategic factors mentions geopolitical an regulatory risk in the DRC (downside), but not the incentive for the USA to ensure strategic control over the resource (upside).

That includes locking in access to Lithium for use by their Industries, and also ensuring China can't further monopolise and manipulate Li price.

The possible value of the Tin and Tantalum aren't included in the simplistic valuation.

No mention of how operating margin is calculated or compared to other resources. We can shovel this stuff off the surface at Manono.

Also nothing about Saudis looking for investment into a longer term easily accessed energy based replacement for oil.

I don't think they've priced in the strategic value of the asset at all, and overstated the geopolitical risk given that the interested parties can exert a lot more influence than AVZ can. Especially given our impotent and disinterested Government.

From the article above

AVZ would be batshit crazy to stop ICC/ICSID until money is in the bank. We’ve been burnt by promises too many timesWe're still continuing down the road of ICSID just in case. Says to me a deal isn't done quite yet

Probably done by RioLOL What a total crock of shit.

Also no one is putting that much effort into creating a website for a lowball valuation unless they're being paid to do it.

So our new low-ball anchor price has moved from 0.60c (from the random journalist) to $1.35 from some random git who i speculate is being paid to try and set low expectation. Keep doubling it a few more times and we'll start getting somewhere.

Strange carry on indeed, something is worth whatever someone is willing to pay for it, isnt that what they sayLOL What a total crock of shit.

Also no one is putting that much effort into creating a website for a lowball valuation unless they're being paid to do it.

So our new low-ball anchor price has moved from 0.60c (from the random journalist) to $1.35 from some random git who i speculate is being paid to try and set low expectation. Keep doubling it a few more times and we'll start getting somewhere.