OK guys. Here it is:

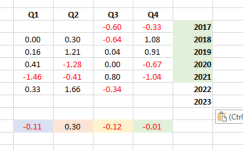

This is the chart showing the UPDATED (Q21) Quarterly model:

View attachment 35558

As you can see, yesterday's data gives the last quarterly BTM sales value as just below the projection.

When the FY23 yearly projection is recalculated it moves from the previous $55.4m sales to a new projection of $54.6m sales.

Pretty much what the share price ended up reflecting - a marginally lower value (excluding all other information in the report that could be speculated on.)

I did note however that BARDA had jumped significantly so my yearly revenue projection has remained pretty constant at $59.8m

If people are not happy with the growth rate in that trendline then they should look elsewhere. Of course they will find nothing like it, with the low levels of risk that PNV offers.

Disclosure: I traded that spike for a nice profit. I'm still trying to catch up with those of averages under $1 ...lol

Happy to answer questions.

...